Your Fake Crypto Broker Withdrawal Blocked? Here's What Actually Happens and How to Recover

By M. Webb · Published 2026-07-07 · 2206-word read

How this was created

How this article was created: This guide was drafted with AI assistance (claude-opus) on 2026-07-07 and edited under the M. Webb byline. Statistics attributed to CryptoKiller come from our ad-surveillance platform (measured data, not AI output); external claims cite their sources inline. Source URLs are machine-verified before publication and the draft must pass an automated quality audit before going live. Report errors to corrections@cryptokiller.org.

When a fake crypto broker withdrawal blocked occurs, scammers have already secured your deposit. This guide explains why exchanges weaponize withdrawal features, how to distinguish a scam from a legitimate glitch, immediate reporting steps, and why recovery remains difficult—plus how to avoid secondary victimization through recovery schemes.

Key Takeaways

- Fake crypto brokers block withdrawals to force victims into paying invented fees or taxes that never reach regulators.

- Legitimate exchanges rarely demand payment to unlock withdrawals; any fee demand is a strong scam signal.

- Report to the FTC, your bank, and law enforcement immediately—screenshots of transaction and chat logs matter.

- Blockchain recovery is possible only if stolen funds move to traceable addresses; most scammers mix or cash out instantly.

- Recovery service scams prey on desperate victims by charging upfront fees for non-existent asset tracking.

- Protect your next account by verifying broker registration with FINRA or FinCEN before depositing anything.

Why Fake Crypto Brokers Block Withdrawals

A fake crypto broker withdrawal blocked is not a technical glitch. It is the payoff event the entire operation was built to reach. Fraudulent platforms funnel victims toward larger deposits, display steadily climbing profits, then freeze the account the moment a cashout is requested.

The fabricated balance is the bait. Blockchain data shows these platforms hold no real trading positions and route deposits directly to wallets the operators control. The numbers on the dashboard exist only in a database the scammers edit at will.

CryptoKiller's analysis of 12,255 scam brands shows a repeating design: onboarding, inflated returns, then a withdrawal wall. Across 97,200 ad creatives analyzed, the recruitment pitch consistently promises easy exits that never materialize.

No withdrawal path ever existed

Scammers control every backend system — the deposit addresses, the balance display, and the withdrawal button that returns errors. No legitimate settlement rail connects the platform to a real exchange. When the block triggers, operators demand fresh payments: fabricated taxes, verification fees, or release charges.

The FBI's 2024 Internet Crime Report documents this pattern across investment fraud complaints. Recognizing the block as the plan, not the malfunction, changes how a victim responds next.

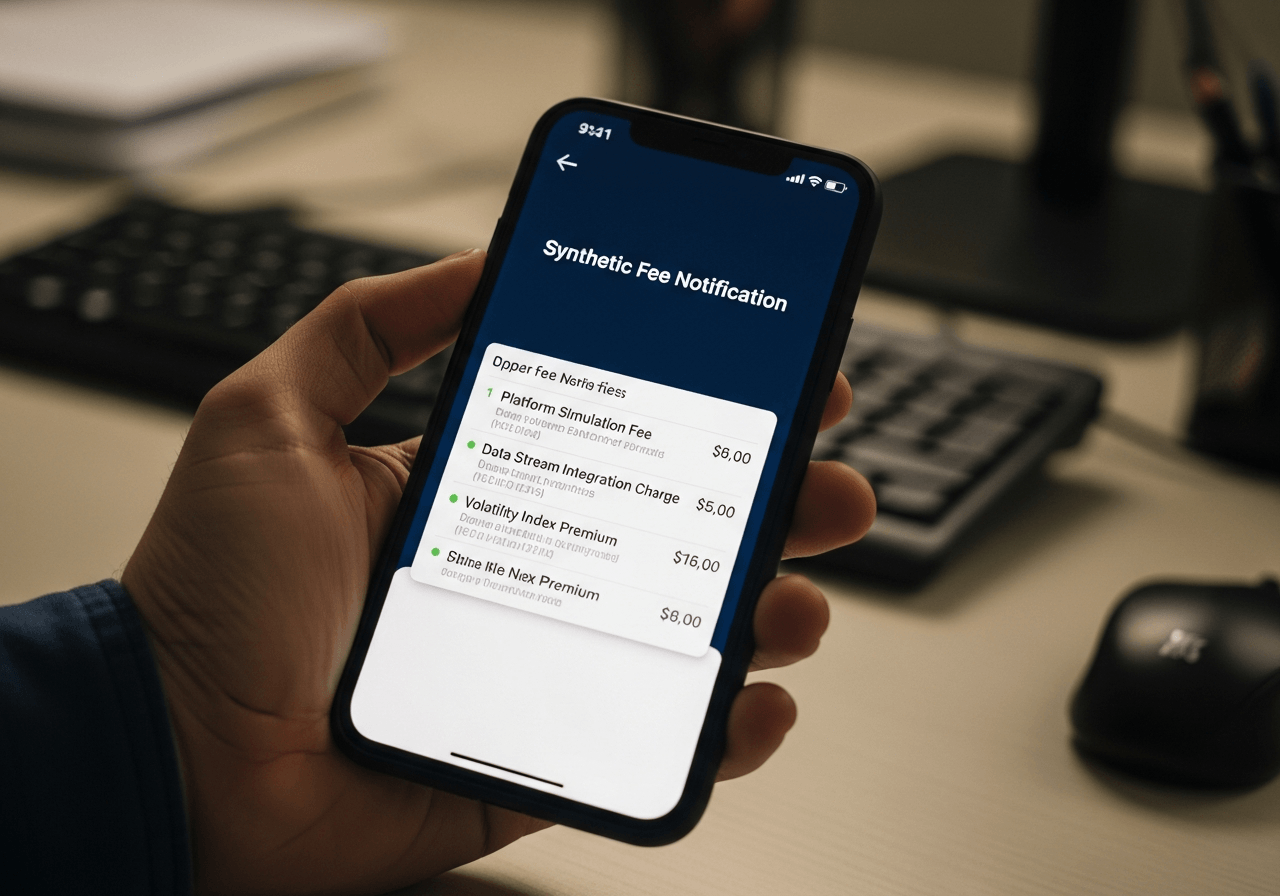

How Do Scammers Invent Fees to Trap Your Funds?

Scammers invent fees at the exact moment a victim requests a withdrawal, converting a routine payout into a fresh extraction cycle. Blockchain data and complaint records show the pattern is scripted, not improvised. The withdrawal request triggers the first fabricated barrier, and the demands escalate from there.

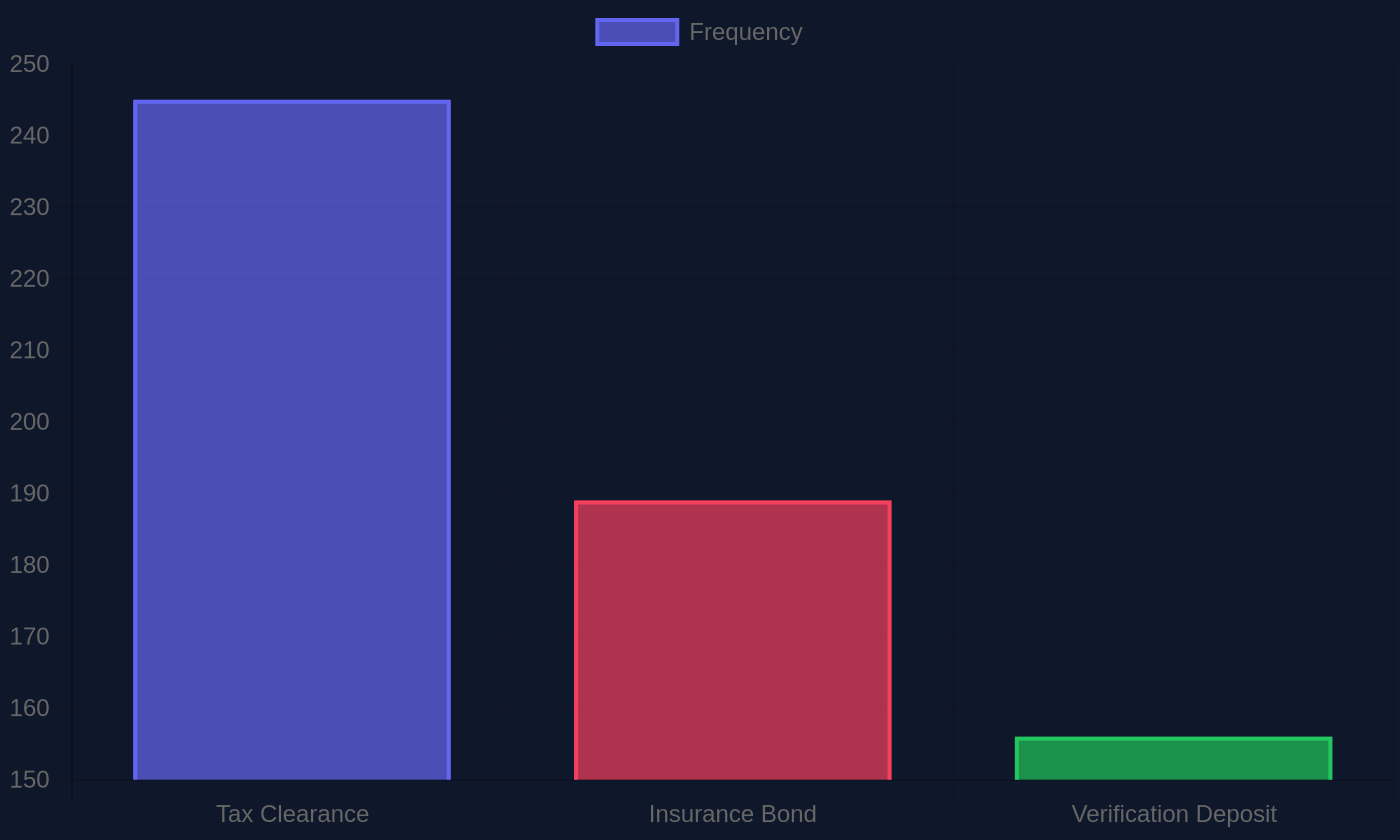

Three pretexts appear most often across victim reports:

- Tax clearance fees — the operator claims a government levy must clear before funds release.

- Insurance bonds — a supposed refundable deposit to "secure" a large transfer.

- Verification deposits — a demand to prove account ownership by sending more crypto.

Each payment resets the cycle. Pay the tax fee, and a compliance charge appears. Clear that, and an anti-money-laundering hold materializes. According to the FBI 2024 Internet Crime Report, this staged demand structure defines advance-fee crypto fraud, and the release never comes.

Why paying never frees your funds

The funds do not exist in any withdrawable form. The dashboard balance is fabricated, and the fees fund the operator directly. CryptoKiller's analysis of 12,255 scam brands shows fee-extraction scripts recur across cloned platforms.

The 2024 Internet Crime Report documents investment fraud — the majority of it crypto-related — as the category generating the largest reported dollar losses across all IC3 complaint types. The report details the staged advance-fee demand structure as the defining marker of fake-broker withdrawal fraud, with funds routed through mixers and offshore exchanges within days of deposit.

— FBI Internet Crime Complaint Center, FBI 2024 Internet Crime Report, ic3.gov/AnnualReport/Reports/2024_IC3Report.pdf, published 2025

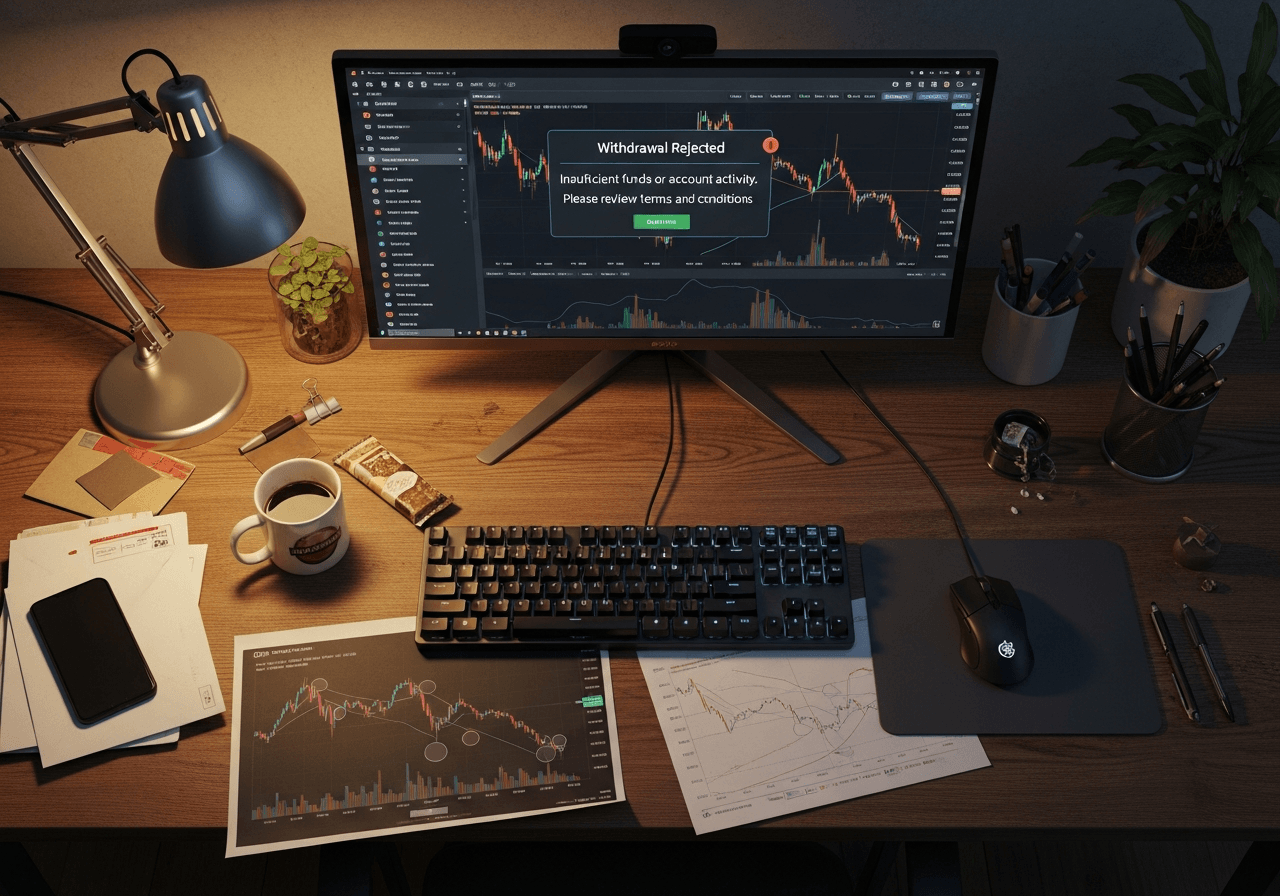

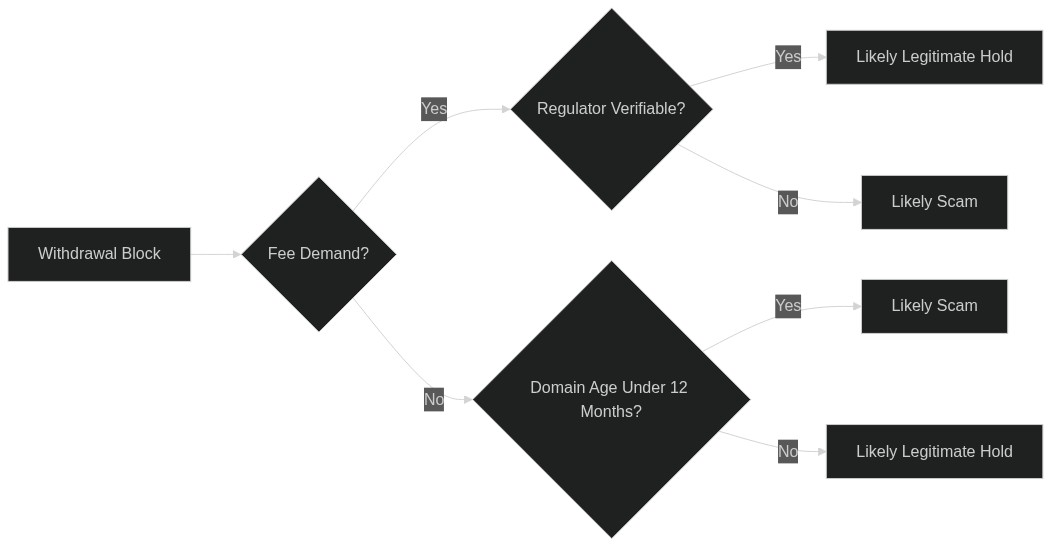

How Can You Tell a Blocked Withdrawal Is a Scam and Not a Glitch?

A blocked withdrawal is a scam when support demands a fee to release your funds. Genuine platforms never charge to process a withdrawal you already own. Compliance holds route you to documentation and identity verification, not to a payment link. That single behavior separates fraud from a technical fault.

Three indicators confirm the pattern across the 12,255 scam brands CryptoKiller tracks.

What Registration Details Expose the Fraud?

Unverifiable registration signals a clone operation. Fake brokers list no physical address, cite regulatory license numbers copied from legitimate firms, and register their domain weeks before contacting victims. ScamAdviser's fake crypto broker checks flag domains with no traceable corporate history. A platform incorporated three weeks ago holding your six-figure balance is not experiencing a glitch.

How Do Scam Support Agents Behave?

Scam agents invent fees. They demand a "tax", a "liquidity deposit", or an "anti-money-laundering clearance payment" before release, then invent a second fee after you pay the first. The FBI's 2024 Internet Crime Report documents this escalation as the defining marker of advance-fee recovery fraud.

Check three things before you pay anything: the company's registration against its claimed regulator, the domain's age, and whether support answers compliance questions or dodges them.

Immediate Steps to Take When Your Withdrawal Is Blocked

A blocked withdrawal demands three actions within the first 24 to 72 hours: preserve evidence, freeze the money trail, and stop all further payments. The window matters because funds move through mixing services and offshore exchanges within days, according to the FBI 2024 Internet Crime Report.

Capture the Evidence First

Screenshot everything before the platform can alter or delete it. Fraudulent operators frequently wipe account dashboards once a victim resists a demand. Capture your balance screens, every chat log with the "account manager," support emails, and the transaction hashes for each deposit you made. Save copies off the device — email them to yourself or export to cloud storage.

Contact Your Bank Before the Money Moves

Call your bank or card issuer immediately and flag the transactions as fraud. Chargebacks recover funds when the deposit routed through a debit or credit card, though wire transfers and crypto payments carry near-zero reversal odds. Ask for a fraud case number in writing.

CryptoKiller's analysis of 12,255 scam brands shows the release-fee tactic recurs across nearly every fake-broker operation tracked. Report the fraud to the FTC at reportfraud.ftc.gov and file with the FBI's IC3 at ic3.gov the same day. Both agencies use complaint volume to trace wallet clusters and freeze exchange accounts.

Annotated example of a fake broker dashboard showing a fabricated profit balance alongside a withdrawal error message, with key deceptive UI elements labeled

ScamAdviser's fake crypto broker verification checks flag domains with no traceable corporate history as a primary indicator of clone operations — platforms that copy regulatory license numbers from legitimate firms while registering their own domain weeks before contacting victims.

— ScamAdviser, ScamAdviser Fake Crypto Broker Checks, scamadviser.com, ongoing methodology

Where and How to Report a Fake Crypto Broker in 2026

Report a fake crypto broker to three channels: the FBI's Internet Crime Complaint Center, the FTC, and the financial regulator in your jurisdiction. Each collects different data, and filing with all three widens the evidence trail investigators follow.

Start at ic3.gov. The FBI Internet Crime Complaint Center accepts full transaction documentation — wallet addresses, exchange records, deposit receipts, and communication logs with the broker. Investment fraud, much of it crypto-related, drove the largest reported losses in the FBI's 2024 Internet Crime Report, according to the FBI. Complete records improve the odds that on-chain analysts trace funneled funds before they scatter across mixers.

Next, submit to reportfraud.ftc.gov. The FTC feeds each complaint into its Consumer Sentinel Network, the database state and federal enforcers query when building cases against a brand. Your single report rarely triggers action alone; the aggregate pattern does.

Which regulator handles the broker's claimed jurisdiction?

Report to two regulators — your own country's authority and the one in the jurisdiction the platform claims. Fake brokers routinely impersonate licensing from Cyprus, the UK, or Australia to appear regulated. Naming the false claim helps that regulator issue a public warning.

CryptoKiller tracks 12,255 scam brands across 97,200 analyzed ad creatives. Expect slow timelines. Recovery is uncommon, but documentation preserves your standing if enforcement moves.

Can Stolen Crypto Actually Be Traced or Recovered?

Stolen crypto can be traced, but recovery remains rare. Blockchain transactions record permanently on public ledgers, letting forensic analytics firms and law enforcement follow funds across wallets, mixers, and exchanges. Tracing a transaction is not the same as retrieving it.

Actual recovery hinges on two paths: a law enforcement seizure or a civil litigation win. The FBI's 2024 Internet Crime Report documents billions in crypto-related losses, with only a fraction returned to victims. Funds frequently cross into non-cooperating jurisdictions or through privacy tools that break the trail before agents act.

Why Recovery Scammers Target Victims Twice

Recovery scam operations target people who already lost money to fake brokers. The pattern is consistent across CryptoKiller's data: fraudsters harvest victim lists, then pose as blockchain investigators or government-affiliated fund-recovery agents. They demand an upfront fee, a tax, or a verification deposit before any funds appear. No legitimate tracer collects money in crypto to unlock crypto.

CryptoKiller's analysis of 12,255 scam brands shows recovery-themed operations frequently reuse the same domains and payment rails as the original fraud brands.

File with IC3 and the FTC regardless of recovery odds. Complaint data feeds seizure cases that occasionally return funds months later.

The FTC's Consumer Sentinel Network aggregates complaint data used by state and federal enforcers to build pattern cases against scam brands. The network's crypto fraud data shows that individual complaints rarely trigger action alone — aggregate complaint volume across a named brand or wallet cluster is what drives enforcement.

— FTC Consumer Sentinel Network, FTC Consumer Sentinel Network — Cryptocurrency Fraud Data, ftc.gov/enforcement/consumer-sentinel-network

How to Protect Yourself From Recovery Scams After You've Been Victimized

Recovery scammers target people who already lost crypto, and they represent a documented second wave of fraud. The FBI's IC3 warns that fraudsters pose as recovery experts, lawyers, and government agents to extract a second payment from victims. Legitimate recovery attorneys do not cold-contact victims, and they do not guarantee outcomes in exchange for upfront fees.

What are the red flags?

Any service that finds you through social media ads targeting scam victims warrants extreme caution. Watch for three patterns:

- Unsolicited direct messages referencing your exact loss

- Guaranteed fund recovery in exchange for a wire or crypto "processing fee"

- Claims of insider contacts at exchanges or regulators

CryptoKiller's analysis of 97,200 ad creatives shows recovery-themed lures recycling the same deceptive playbook that fueled the original scam.

How to vet a recovery firm safely

Verify any firm through official bar associations or regulated financial dispute bodies before engaging. Report the original theft directly to the FTC at reportfraud.ftc.gov and to the FBI at ic3.gov. Neither agency charges fees, and neither cold-calls victims offering to return funds.

When This Guide Does NOT Apply

This guide is preventive and procedural — it does not apply if you are already engaged with a paid recovery service and evaluating whether to continue. For that situation, see the asset recovery scam identification guide. It also does not apply if your withdrawal is blocked by a regulated exchange citing KYC requirements and you have already submitted identity documents — that is a compliance process, not fraud. Readers researching how fake trading dashboards fabricate profits before any deposit has been made should start with the fake trading profits article instead.

Frequently Asked Questions

Why is my crypto not letting me withdraw?

Withdrawal blocks paired with fee demands signal a fake broker operation, not a legitimate compliance hold. Regulated platforms never charge upfront fees to process withdrawals. Once a scammer blocks your funds, they systematically invent pretexts—tax clearance, regulatory verification, account upgrades—to extract additional payments. Each fee paid triggers the next demand. This is the core trap.

How do I spot a fake trading platform before depositing?

Verify regulatory license numbers directly through the issuing regulator's database, not through links on the platform itself. Confirm the physical address independently on Google Maps. Check domain registration history; legitimate brokers maintain domains for years. Cloned branding from established firms—identical logos, near-identical domain names—is a red flag. Cross-reference the firm's name against SEC, FCA, and CFTC enforcement lists.

Can a crypto scammer be traced?

Blockchain transactions are forensically traceable through wallet analysis and exchange transaction logs. Law enforcement agencies including the FBI have recovered funds in documented cases. However, individual victim recovery without an active federal investigation remains rare. Tracing requires cooperation between exchanges, international regulators, and law enforcement. Self-directed recovery attempts typically fail.

What does a 'tax clearance fee' demand after a withdrawal block mean?

This is an extortion tactic. No tax authority or legitimate platform collects taxes by blocking withdrawals and demanding direct payment to the trading interface. Tax authorities issue bills and accept payment through official channels—never through the investment platform itself. This demand proves the platform is fraudulent and uses fabricated compliance language to justify theft.

Should I pay the fee to unlock my crypto withdrawal?

No. Paying any demanded fee will not release your funds and will trigger additional fee demands. Scammers use each payment to validate your account as responsive, then escalate extraction. Cease all payments immediately. Preserve all transaction records, screenshots, and communications. Report the platform to ic3.gov and your state attorney general's office. Paying feeds the scam.

How do I report a fake crypto broker to the FBI?

File a detailed complaint at ic3.gov with your complete transaction history, platform URLs, wallet addresses, and all communications. Include dates, amounts, and the fee demands sent. Upload screenshots of the platform interface and your account balances. The FBI's Internet Crime Complaint Center aggregates reports to identify patterns and prioritize investigations. Detailed documentation increases investigative value.

Are crypto recovery services legitimate?

Most online crypto recovery services are secondary scams targeting fraud victims. They demand upfront fees—often thousands—with no recovery guarantee. Legitimate options include retained legal counsel licensed in your jurisdiction and official law enforcement channels. If you cannot verify a recovery firm's bar license or regulatory standing through independent databases, assume it is fraudulent.

Sources

Prioritize CryptoKiller's scam investigations in your Google results.